Producer Company Registration in India

For generations ,India’s economy has been predominantly agrarian ,with around 60% of its population depending on agriculture for sustenance. Despite its significance ,the agricultural sector and farmers have encountered various obstacles and difficulties over time.

In response to these challenges, the Government of India formed an expert committee led by economist Y.K. Alagh to assess the situation. In 2002, based on the committee’s recommendations, the concept of producer companies was introduced in the Indian economy. Since then, these producer companies have played a vital role in assisting primary producers by enabling them to access inputs, credit, production technology, markets, and other essential resources.

The primary objective of producer companies is to empower and uplift primary producers by bringing them together as collective entities. These companies operate based on cooperative principles, enabling farmers and other primary producers to pool their resources and collaborate for mutual advantages. Through this approach, they can strengthen their bargaining position, access improved markets, enhance productivity through shared knowledge and technology, and overcome the various challenges associated with individual farming or production efforts.

The establishment of producer companies has been a crucial measure in tackling the challenges confronted by primary producers in India. It has offered them a platform to come together ,pool resources, and take advantage of economies of scale ,leading to enhanced income levels and overall well-being. By fostering collaboration and resource-sharing, producer companies have contributed to the improvement of the livelihoods of primary producers and their economic prospects.

Producer Company

A producer company is a legally recognized entity comprising farmers or agriculturists who come together to improve their living standards and enhance the support ,income ,and profitability of their activities. As per Section 465(1) of the Companies Act, 2013, the provisions governing Producer Companies under Part IXA of the Companies Act ,1956 ,continue to apply. Accordingly ,a Producer Company can be formed by a minimum of 10 individuals or 2 institutions or a combination of both (i.e., 10 individuals and 2 institutions) with specific business objectives as defined by the Act.

A farmer producer company is a unique blend of private limited companies and cooperative societies, registered under the Act. It operates with a democratic governance model, where every member or producer enjoys equal voting rights, regardless of the number of shares they hold.

Objectives of the Producer Company

The primary goal of a farmer producer company is to enable the establishment of cooperative businesses in the form of companies and allow existing cooperative entities to convert into companies. As per the law ,the objectives of a producer company may include the following matters:

- A producer company’s objectives encompass various activities related to the production, harvesting, procurement ,grading ,pooling ,handling, marketing, selling, export of primary production of its members, or the import of goods or services for their benefit. These activities can be undertaken independently by the producer company or in collaboration with other institutions.

- In addition to the mentioned objectives, a producer company can engage in processing activities ,which include preserving ,drying ,distilling, brewing ,vinting ,canning ,and packaging the produce of its members. These processing activities are aimed at adding value to the primary production of the members and enhancing their overall economic benefits.

- A producer company can also engage in the manufacturing ,sale, or supply of machinery ,equipment ,or consumables primarily to its members. Providing its members and others with education on the concepts of mutual help.

- We Provide a Comprehensive range of Services ,including Technical expertise ,Consultancy ,Training ,research and Development ,and other activities that foster the Growth and welfare of our valued members.

- Our focus lies in actively participating in activities pertaining to power generation ,transmission ,and distribution. We are dedicated to land and water resource revitalization, sustainable utilization, conservation, and effective communication, all in connection with primary produce.

- Insurance coverage for producers or their primary produce.

- Promoting techniques of mutuality and mutual assistance.

- Implementing welfare measures or providing facilities for the benefit of members, as determined by the Board.

- We are Committed to executing Welfare measures and offering facilities that cater to the Well-being of our members ,as directed by the Board.

- A farmer producer company aims to provide financial support for procurement, processing, marketing, and other activities mentioned in clauses (a) to (j). This includes offering credit facilities and other financial services to its members, primarily involved in agricultural production. These objectives showcase the diverse range of activities and services dedicated to supporting the members’ interests, development, and welfare.

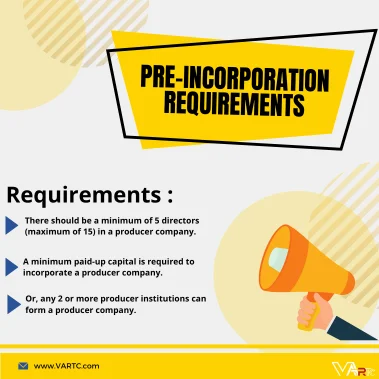

Pre-Incorporation Requirements

- A Production Company can be formed by a group of 10 or more individual Producers. There is no Upper limit on the Number of Members who can Join the Company.

- Or, any 2 or more producer institutions can form a producer company.

- A minimum paid-up capital is required to incorporate a producer company.

- There should be a minimum of 5 directors (maximum of 15) in a producer company.

- A production Company cannot be Converted into a Public company ,but it does have the option to be Converted into a multi-state co-operative society.

Registration Procedure

Registering a Producer Company follows a similar Process to that of a Private Limited Company. The first step involves obtaining Digital Signature (DSC) and Director Identification Number (DIN) for the proposed directors. Once these are obtained ,an application for name reservation is filed with the relevant Registrar of Companies (ROC).

As per the Act, a producer company’s name must conclude with “Producer Limited Company.” After obtaining ROC approval for the suggested name, an application for incorporation is submitted in the prescribed format. The Registrar reviews the application and relevant documents. Upon satisfaction, the Registrar grants approval and issues the Certificate of Incorporation for the Producer Company.

Procedure and Documentation Required to Incorporate a Producer Company

- The initial stage involves obtaining a Digital Signature Certificate (DSC) from all the directors. The documents required to obtain a DSC are:

- PAN Card of the Director

- Aadhaar Card of the Director

- Photo

- Email Id

- Contact Number

- Once the DSC is obtained, the subsequent step is to acquire the Director Identification Number (DIN) by submitting form DIR – 3 or SPICe+ Form, along with self-attested Identity proof, address proof, and a photograph.

- Next, the production company’s name is to be chosen. To finalize the name, Form SPICe+ must be filed with the Registrar of Companies (ROC), providing two preferred names along with their significance. The chosen name must end with the words “PRODUCER COMPANY.”

- After the name is approved by the ROC, the following documents are to be prepared:

- The Memorandum of Association is to be crafted ,encompassing all the objectives that the company intends to pursue

- The Articles of Association is to be Drafted Containing all the by-laws of the company.

- An affidavit must be signed by all the subscribers of the proposed company, declaring their legal competence to act as subscribers.

- To use an individual’s Address as the registered office of the company ,a utility bill and a No Objection Certificate (NOC) must be obtained from the owner. If the Property is not owned ,a lease Agreement will be Attached to the form.

- All the prepared documents will be attached to Form SPICe+ and uploaded on the ROC website. After thorough verification ,the ROC will issue a Certificate of Incorporation ,allowing the company to commence its business operations.

This form of establishment empowers Primary producers from low-income groups to maximize their income through collective bargaining and direct Sales of Products to consumers.

Authorized Activities for Producer Companies

The Producer Company is mandated to handle the produce of its members and has the authorization to conduct any of the following activities:

- The Producer Company is involved in the processing of its members’ produce ,which encompasses activities such as preserving ,brewing ,vinting ,drying ,distilling ,canning ,and packaging.

- The Producer Company engages in the manufacturing ,sale, or supply of equipment ,machinery ,or consumables to its producer members.

- The Producer Company’s objective is to offer education on mutual assistance principles to its producer members and others.

- The Producer Company aims to provide consultancy services, technical assistance ,Training ,research and development ,and all other necessary activities to Promote the interests of its producer members.

- The Producer Company is involved in the generation, transmission ,and distribution of power ,conservation and communication related to primary produce ,as well as revitalization of land and water resources.

- Insurance of the primary produce and its producer;

- To promote the techniques of mutuality and mutual assistance;

- The welfare of members as may be decided by the Board;

- The Producer Company is engaged in financing procurement, marketing, processing, and other activities, including extending credit facilities or providing financial assistance to its producer members.

- The Producer Company may undertake any other activity, ancillary or incidental to its main objectives, to promote mutual assistance among its producer members in alignment with the principles of mutuality.

Note: According to the Companies Act 1956 ,primary produce refers to agricultural produce grown or produced by a farmer. It includes various activities such as animal husbandry, Floriculture ,horticulture ,viticulture ,pisciculture ,re-vegetation, bee raising ,forestry ,forest products ,farming plantation products ,hand-loom and handicraft products, and other cottage industries.

Benefits of Farmer Producer Companies

The following are the benefits enjoyed by a Farmer Producer Company:

- The value of the pooled and delivered output, as established by the directors, will first be distributed to the producer company’s members. This amount will be distributed later in the form of cash, kind, or equity shares.

- In proportion to the shares they own, producer company members will be able to obtain bonus shares.

- After making provisions for limited return and reserves, the surplus may be distributed as a patronage bonus to the members of the producer company. (*A patronage bonus is a reward given to members based on their participation and contributions to the company’s activities.)

A patronage bonus represents the distribution of surplus income to members of the producer company based on their individual patronage. Patronage, on the other hand, refers to the active participation of members in business activities by utilizing the services provided by the producer company.

Loans and Investments

As stated earlier ,the Producer Company is composed of primary producers who may require financial assistance at times. To address this, the Act includes a special provision allowing the company to provide loans to its producer members. Financial support can be extended to members through the following means:

- Credit facility: Any member can avail credit for a Period of up to six months ,which must be in Connection with the business of the Company.

- Loans and advances: The producer members can obtain loans and advances against security ,with repayment due within a period not exceeding seven years from the date of disbursement.

- NABARD Loan: NABARD extends support and financial assistance to cater to the requirements of Producer Companies. In 2011, NABARD established a Rs. 50 crore Producer Organisation Development Fund (PODF) from its operating surplus.

Tax Benefit (Taxability of Producer Company)

The Income Tax Act, 1961 ,under section 10(1) ,grants an exemption for Agricultural income. However ,the exemption provided under section 10(1) may vary based on the Specific agricultural activity being conducted.

The Income Tax Act does not explicitly outline any specific tax benefits or exemptions exclusively for producer companies based on their definition. However, depending on the agricultural activities performed by the producer company, certain tax benefits and exemptions may be accessible.

As an illustration ,income generated from the sale of cultivated green tea leaves is classified as agricultural income under the Income Tax Act, making it entirely tax-free. Nevertheless ,if the tea leaves undergo additional processing for tea manufacturing, only 60% of the income will be considered as agricultural income ,and the remaining 40% will be subject to taxation. Therefore ,the tax benefit and exemption for a producer company are contingent on the specific activities it engages in.

Frequently Asked Questions:

A- Incorporated under the Companies Act, 2013 (previously the Companies Act, 1956) ,a producer company is involved in various activities ,such as producing ,grading ,harvesting, pooling, selling ,marketing ,and exporting the primary produce of its members. Additionally ,they have the privilege to import products and services for the benefit of their members, alongside exporting them.

A- Any primary producer can become a member of the producer company voluntarily, as long as they accept the responsibilities of membership. However, individuals with commercial interests that compete with the producer company are not eligible to join. Members hold equity in proportion to their support. If members cease to be producers or fail to meet membership requirements, the Board of Directors may request them to return their shares in the producer company.

A- To establish a farmer producer company, a minimum of ten producers or two producing institutions are required. There is no upper limit for the number of members in a producer company, providing flexibility for its composition.

A- From the name of the producer company, it may seem that the producer companies are public companies. Still, on the contrary, the Companies Act, 1956, section 581C, suggests that a producer company cannot be deemed a public company and shall become a corporation similar to a private company.

A- The Board of Directors appoints a Chief Executive to run the producer firm. He is accountable for issuing instructions for work to run the organization in the right direction and has great control over the company's decisions. The executive is directly answerable to the Board of Directors for his decisions for the company. The qualifications or experience for the Chief Executive post is taken by the Board of Directors, keeping in mind the provisions contained in the company's articles. The Chief Executive may or may not be a primary producer for the company depending upon the provisions in the articles.

A- The company requires a minimum of ₹5,00,000 as capital to incorporate a producer company.

A- A producer company is run by a Board of Directors who are accountable to the company's members. The board can further appoint a Chief Executive or any person who can give directions or instructions for day-to-day business decisions for the producer company. The initial Board of Directors are the people chosen as directors by the members on the incorporation of the producer company. After that, the board gets elected at the annual general meeting or as required.

A- The Board of Directors appoints a Chief Executive to run the producer firm. He is accountable for issuing instructions for work to run the organization in the right direction and has great control over the company's decisions. The executive is directly answerable to the Board of Directors for his decisions for the company. The qualifications or experience for the Chief Executive post is taken by the Board of Directors, keeping in mind the provisions contained in the company's articles. The Chief Executive may or may not be a primary producer for the company depending upon the provisions in the articles.

A- A producer company should have at least five directors on its board with an upper limit of up to 15 directors.The company can also have additional or expert directors whose number, however, shall not exceed one-fifth of the total strength of the number of directors on the Board.

A- A director shall be appointed for a minimum of one year but not more than five years. Also, every retired director is eligible to be re-elected by the members as a director.

A- The members of a producer company have limited liability for the unpaid share amount. Hence, in the event of liquidation, the personal assets of the members of the company are safe Forming a company allows the members to expand their business by operating their business all over the country, including exports Supply chain management can become easier by making company subsidiaries or entering joint ventures Ownership of the company stays safe with the primary producers. The shares can only be transferred to the company's active members and only after the Board of Directors Accountability of the upper management increases towards the members, and a double check is maintained with regular quarterly meetings and reports Taking business loans becomes easier for farmers as a single entity at a lower interest rate.

A- Forming a producer company from the start can take around 35-40 working days on average.

A- Suppose the producer company’s members consist only of individual members. In that case, the voting rights are exercised as a single vote for each member, irrespective of his equity or patronage in the company If the producer company’s members consist only of producer institutions, then voting rights are determined on the basis of their respective participation in the producer company in the previous financial year. However, in the initial year of registration of the company, the rights are determined based on shareholding in the producer company. If the producer company consists of both individual and producer institutions, the rights to vote are distributed as a single vote for each member.

A- SPICe+ is an integrated Web form for incorporation of a company simultaneously offering 10 services by 3 Central Govt Ministries & Departments. (Ministry of Corporate Affairs, Ministry of Labour & Department of Revenue in the Ministry of Finance) and Two-State Government (Maharashtra & Karnataka), thereby saving as many procedures, time, and cost for Starting a Business in India. SPICe+ is a part of various initiatives and commitments of the Government of India towards Ease of Doing Business (EODB).

The VARTC Team offers top-notch services for Producer Company Registration. If you encounter any challenges, our experts are ready to assist you in achieving your business goals. Contact us for further information and support.